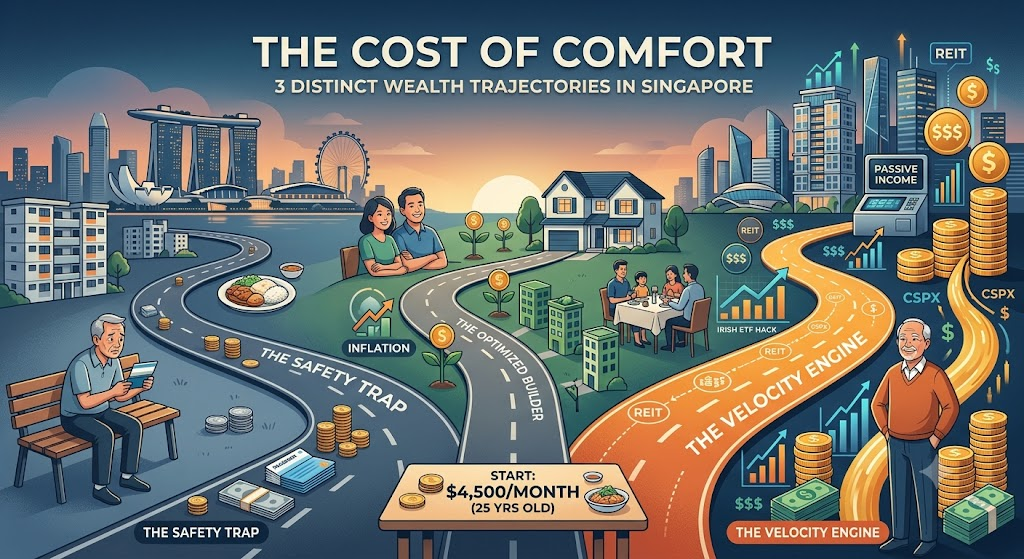

Walk into any CBD hawker center during lunchtime, and you are surrounded by people who share almost identical financial profiles. They are in their mid-20s, earning a respectable starting salary of around $4,500, managing their first HDB flats, and diligently setting aside a few hundred dollars every month.

On paper, they are all doing everything right.

But if you fast-forward three decades, their realities will look completely different. One will be struggling to outpace the rising cost of hawker food and healthcare, one will enjoy a secure, stress-free middle-class retirement, and the third will have engineered a passive wealth machine that replaces their entire working salary.

The differentiator isn’t how much they earn or how hard they work. It’s how they choose to define “risk” early in their careers. Here is a look at three distinct wealth trajectories in Singapore, and the structural mechanics that separate them.

Strategy 1: The Safety Trap (Optimizing for Zero Volatility)

The first path is walked by the hyper-conservative saver. Driven by a desire for absolute certainty, this person builds a standard emergency cushion and routes every extra dollar into capital-guaranteed instruments:

- High-yield bank accounts (like UOB Stash hovering around 2%)

- Fixed deposits locked in at mid-1% rates

- Singapore Savings Bonds (SSB) yielding just over 2%

The 10-Year Outcome (Age 35): Through sheer discipline, they amass roughly $40,000 in liquid cash. Combined with their mandatory CPF ordinary and special account contributions, their total net worth sits around $140,000. They feel incredibly secure because their account balances never go down.

The Retirement Reality (Age 65): What this strategy ignores is the silent tax of inflation, which historically runs at 2% to 2.5% in Singapore. By matching inflation rather than beating it, their purchasing power completely stagnates. By age 65, they will have hit their Full Retirement Sum (FRS), yielding a CPF Life payout of roughly $1,780 a month.

While this clears the baseline $1,492 monthly requirement for elderly singles calculated by the Lee Kuan Yew School of Public Policy, it leaves absolutely zero margin for error. A single uncovered medical bill or a desire to travel completely breaks the budget. In trying to avoid short-term market drops, they locked themselves into a long-term financial ceiling.

Strategy 2: The Optimized Builder (Mitigating the Global Tax Drag)

The second path is taken by someone who understands that true safety means beating inflation, not just matching it. They maintain a lean cash buffer but route $400 a month into low-cost global equity indexes, backed by a strategic use of Singapore’s retirement infrastructure.

This investor stands out by mastering two specific mechanics:

- The Irish ETF Hack: Rather than buying popular US-domiciled ETFs like VOO or SPY—which subject Singaporeans to a hefty 30% dividend withholding tax—they buy Irish-domiciled equivalents like CSPX. This leverages the US-Ireland tax treaty, cutting the dividend tax drag perfectly in half to 15%. Combined with Singapore’s 0% capital gains tax, their growth compounds far more efficiently.

- Guaranteed 4% Compounding: They aggressively maximize the Retirement Sum Topping Up (RSTU) scheme, putting $6,000 a year directly into their CPF Special Account (SA). This grants them immediate income tax relief while letting the cash compound at a government-backed 4% to 5% rate with absolutely zero market risk.

The Multiplier Effect: By age 35, this balanced approach yields a net worth of $265,000—creating an immediate $125,000 gap over the conservative saver using the exact same salary. By age 65, their portfolio matures into a $1.1M+ nest egg. Combined with CPF Life and high-yielding local REITs, they enjoy a highly flexible retirement income of $3,500 to $5,000 every single month.

Strategy 3: The Velocity Wealth Engine (Maximizing Legal Leverage)

The final path belongs to the investor who treats their youth as an aggressive leverage tool. They view market downturns not as a crisis, but as a systematic wealth transfer.

- The Triple Tax Shield: From their very first paycheck, they utilize the Supplementary Retirement Scheme (SRS) to its maximum statutory limit ($15,300 for citizens). Every dollar lowers their current year income tax bracket, compounds entirely tax-free inside equity ETFs, and qualifies for a 50% tax exemption upon withdrawal in retirement.

- The Tipping Point: They automate aggressive monthly contributions into global equities, buying even heavier when headlines claim the sky is falling.

By age 45, their equity portfolio hits roughly $800,000. At a standard 9% annualized market return, that portfolio quietly generates $6,000 a month in pure growth.

At this exact intersection, their invested capital officially earns more passive income each month than their actual day job paid them when they entered the workforce.

By age 65, this investor sits on a diversified stock and REIT asset base worth between $3.5M and $5M. With an Enhanced Retirement Sum (ERS) CPF Life payout, their total monthly cash flow sits between $13,000 and $18,000.

Actionable Steps: Moving Beyond Inertia

Every single one of these paths requires discipline. The difference in the final destination isn’t a matter of effort; it’s a matter of architectural design. If you want to transition your wealth from standing still to compounding exponentially, start with two structural adjustments this week:

- Audit Your CPF Leakage: Log into your CPF portal. If you have significant capital sitting in your Ordinary Account earning 2.5% that you don’t intend to use for a housing mortgage anytime soon, evaluate moving it to your Special Account or executing an RSTU top-up to capture the guaranteed 4% compounding before the calendar year ends.

- Eliminate Dividend Drag: If you are building a long-term portfolio via a brokerage like Interactive Brokers or Tiger, ensure your core global equity holdings are domiciled in Ireland (look for funds like CSPX or VWRA) to permanently shield your dividends from unnecessary international taxation.

True financial risk isn’t watching your stock portfolio fluctuate during a bad quarter. True risk is watching your savings account stay perfectly flat for forty years while the world moves on without you.

*** SEE MY TRADES & PORTFOLIO ON PATREON ***

If you are interested to find out more about my trades, what shares I am buying/ selling or which options contracts I have opened/ closed, I will be updating them on Patreon (on the same day I made the trades), so do follow me there if you need some reference or inspiration.

Click here to access my Patreon page

*** FOLLOW US ON SOCIAL MEDIA ***

Follow me on Facebook and LinkedIn, to get notified of my latest posts on social media. Or subscribe to my blog (scroll to the bottom of the page) to have my new posts sent directly to your mailbox.

We also have a community passionate about investing, trading, and personal finance over our Telegram or Facebook group. So, join us there for a good discussion, post queries, or simply share your financial knowledge.

*** FREE BEGINNER GUIDE TO OPTIONS TRADING ***

Keen to learn about options trading but do not wish to pay for expensive courses, this newbie guide will help gain the knowledge and fundamentals to understand options better. And it’s totally free!

The Newbie’s Guide To Options Trading

*** FREE MOTIVATIONAL BOOK ***

If earning more money from your investment does not excite you anymore, you may be seeking a purpose that brings fulfillment and meaning in life. I have written a motivational book that may be useful to you in some ways.

Click here to download my motivational book

*** BUY ME A CUP OF COFFEE ***

If my blog has benefited you in some ways and you would like to offer a token of appreciation, you may do so via this page. Thank you very much for your support!

Click here to support the site

*** MUST-READ BLOG POSTS ***

The day that I lost everything….

I Was Margin Called, IBKR Liquidated ALL My Positions & Realised S$540k (USD400k) Worth Of Losses

Sharing these 6 fatal mistakes in investing and options trading so you can avoid these pitfalls

The 6 Fatal Investing/ Trading Mistakes That Made Me Lose More Than $1M

After accumulating more than 600k of unrealized losses on my portfolio, I wrote this article to encourage friends and investors who are also losing a lot of money to the market.

If You Are Feeling Depressed From Losing Lots Of Money In The Stock Market, Here’s An Article For You

The precious 6 lessons I learnt after cutting more than half a million of losses in the stock market through bad investments and risky trades.

6 Lessons Learnt After Losing 551k In 10 Years Of Investing & Options Trading | What Newbies Should Know They Start Investing/ Trading

In the 10 years of my investing journey, I have made many mistakes but also learned many lessons from these mistakes. I compiled the 10 most valuable lessons that I have learned and may they help you succeed in your investing journey.

Happy 10 Years Of Investing | 348k (Realised) Profit, 635k (Unrealized) Loss & 10 Lessons Learnt

How I managed to build a 1M investment/ trading portfolio despite coming from humble beginnings.

How A Poor Kid Got To A 1M Investment Portfolio | Tips & Principles Of Building Wealth

I did these 10 side hustles while holding a full-time job, so I share them here so you can be inspired to grow your wealth through a side hustle that you enjoy.

I Did These 10 Side Hustles While Working Full Time | 10 Side Hustle Ideas To Help You Earn An Extra Income

Struggling with inflation and high cost of living? Try these 10 methods to help you save money and accumulate more savings for investments or rainy days.

10 Ways To Save Money To Help You Fight Inflation & Rising Costs Of Living

Why I am building $120,000 of cash reserves in Singapore Savings Bonds (SSB) & 5 reasons why I think SSB is a worthy low or zero-risk investment that you can consider.

Why I Am Building $120,000 Of Cash Reserves In Singapore Savings Bonds (SSB)? | 5 Reasons Why SSB Is A Worthy Low-Risk Investment