The Singapore Savings Bonds (SSBs) are a type of Singapore Government Securities that are issued for investors who want to participate in the Singapore Government Securities (SGS) market but in smaller denominations.

The capital is guaranteed (you won’t lose what you have invested), the interest payout is guaranteed (fixed at the time of purchase) and will reach maturity after 10 years. However, it can be redeemed any month (partial or full) during the 10 year tenure at a minimum multiple of $500. Each person is allowed to purchase up to $200,000 worth of SSBs.

The first interest payout is 6 months after the bond is assigned. For early redemption/ withdrawal, the interest will be pro-rated accordingly.

Reaching 120K Target

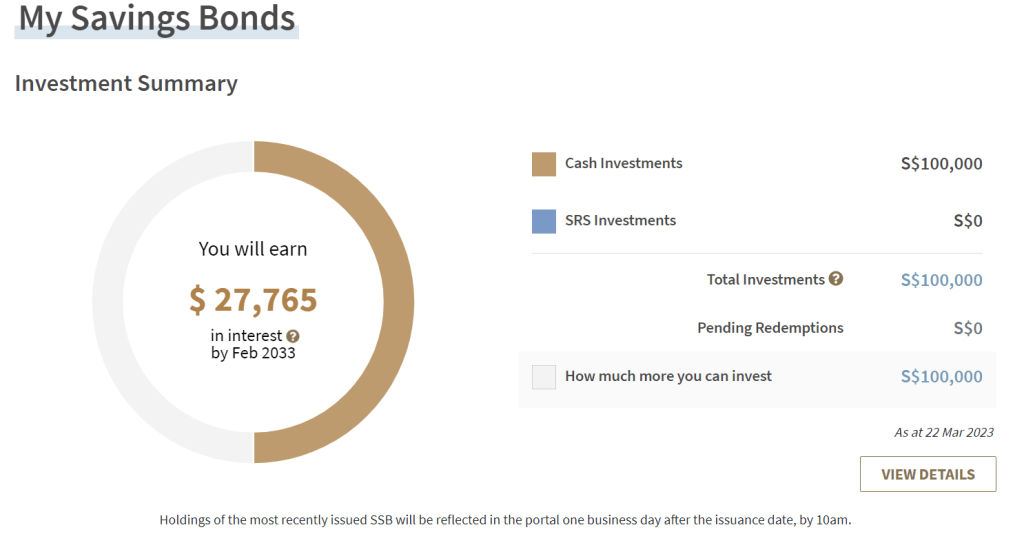

At this time of writing (March 2023), I have already bought $100,000 worth of SSBs.

I have applied for another $20,000 this month and if it gets assigned, I would have reached my target of owning $120,000 worth of SSBs.

5 Reasons Why I Plan To Park $120K In SSBs

There are 5 reasons why I choose to accumulate $120K worth of SSBs.

Reason 1: Safe & Reliable Store Of Wealth

As SSB is backed by the Singapore Government (you are essentially lending money to the Singapore Government), it is a safe storage of cash reserves. The capital is guaranteed and has a very low risk of disappearing into thin air. Singapore has great sovereign ratings and is the safest possible place to park your money.

Why Not Shares?

There was a stage where I thought of parking my cash reserves in shares, in particular the most valuable companies in the world (which have low risk of bankruptcy). However, putting money in shares is nice if there is capital appreciation or where there is a consistent payout of dividends and the share price is maintained.

On the flip side, share investments come with the risk of capital depreciation, i.e. share losing value and may never return for a long time. If you pick the wrong stock, you may lose all your money even if you have years of holding power.

Reason 2: Easy Withdrawal & Short Withdrawal Lead Time (Good For Emergency Purpose)

In the event of emergency, it is easy to withdraw and takes at most a month to obtain the funds. It is not locked like Fixed Deposit (FD) or has any penalty against early withdrawal.

You can apply to redeem your Savings Bonds as early as the month in which the bond is issued. Redemption proceeds will be paid out by the 2nd business day of the following month.

The longest wait to redeem the bond happens when you redeem on the first day of the month and you will only get your cash + interest on the 2nd day of the next month. The shortest wait is when you redeem on the fourth last day of the month and you get paid about a week later (on the 2nd day of the following month).

I will be using whatever cash I have on hand to tide though that period (between a week to a month), before fresh funding comes back into my bank account via the redemption of my SSBs.

Reason 3: Interest Guaranteed For The Next 10 Years

In the current high interest rate environment, the returns from SSB (even at highest of average 3.26% per annum for 10 years) may not seem too attractive for some. However, the high interest rate environment will not last forever. In the latest FOMC meeting on 22 March 23, the Federal Reserves has already planned to cut interest rate from 2024 onwards, if inflation is under control.

When the Fed cuts the interest rate, say in 2024 or 2025, the interest offered by the various institutions, though Fixed Deposits or high interest savings accounts, will revert back to lower rates, just like the days of the pandemic.

For SSB, the interest rate is secured beyond 2024 or 2025, all the way to maturity date, even if interest rate remains low for the years to come.

If you have bought this month’s bond (issued on April 23), you would have gotten more than 3% annual interest up to 2033 (see table below).

Reason 4: Regular Source Of Passive Income

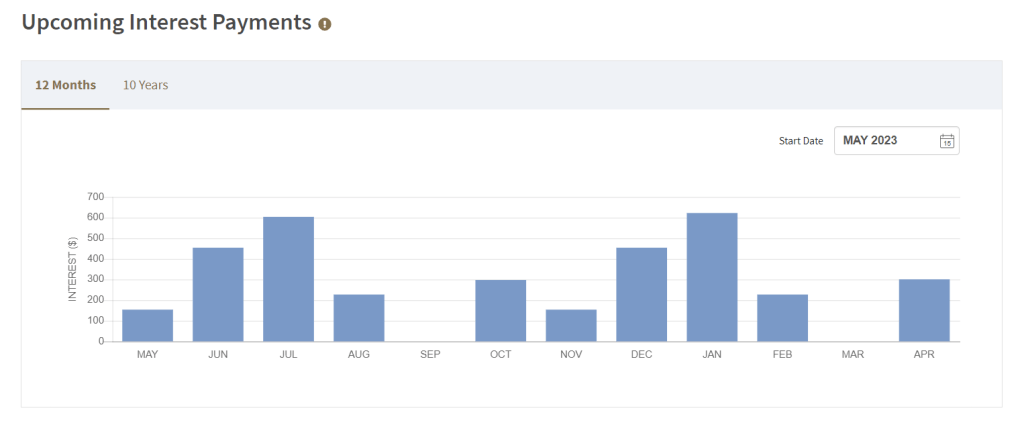

I staggered my SSB purchase over the various months so that when the payout of interest (which occurs every 6 months), will happen on different months instead of only two months of the year. By doing so, I can also wait average out the interest as some months gave out better interest rates.

The below table shows my current payout for the next 12 months. If I do not redeem any bond, this will be the payout for the next 10 years.

If that 20k SSB that I have applied this month is successful, then this will be the new payout schedule and amount. So, with 120k worth of investments, I will get between $150 to $600 per month for 10 months in a year.

Reason 5: Transferrable & Easy To Handle If I Die (Prematurely)

I currently have about 495k of capital in shares (mostly US shares), 46k in options and my US shares also double up for me to sell options. However, all these stuff about options trading and shares investment are like rocket science to my spouse. So, if I pass away prematurely or suddenly, she would not have the knowledge or interest to continue this kind of investment/ trading style.

Unlike shares investment and options trading, SSB is transferrable and easier to manage for my spouse as she is owning some SSB on her own. Even my 70-year-old MIL can understand how SSB works, how to apply and redeem.

I think this contingency planning on how to pass on our assets and investments is important as our loved ones may not know how to handle all these securities when they receive it. So, it is good to Keep It Simple Stupid (KISS).

How Long Can 120K Last For My Family?

Based on the lazy and quick method that I used to calculate my monthly expenses, I will need around $4,000 to sustain my family’s current lifestyle.

Reference Article:

How Much Is Enough For Retirement Or Emergency Funds? | How I Calculate My Monthly Expenses

So, with 120k as a reserves fund, it will be enough to tide through for 30 months or 2.5 years. This will be helpful in the event I lose my main source of income, e.g. losing my current job.

This 120k is also my fail-safe mechanism to guard my last piece of wealth, just in case I go crazy and decide to YOLO all my cash on hand away in trading or other high risk financial instruments.

Concluding Thoughts

I hope you find this sharing useful and can help you better manage your wealth and savings in 2023 and beyond. If you are looking at a place to park your cash reserves, be able to withdraw in a short period of time and get higher interest than the banks, then SSB is a good consideration as it is capital guaranteed and interest guaranteed until the bond matures in 10 years, or when you decide to cash them out, whichever is earlier. The above 5 reasons may also be relevant to you.

*** Update on 13 April 23 ***

My $20,000 SSB application in March was assigned and I have reached my target of $120k in SSB.

My interest payout (passive income) over the upcoming months would be as follow:

Over the next 10 years (at least 3k per year starting from 2024 onwards)

<< Subscribe to my blog to have all these articles delivered directly to your email address >>

*** FREE MONEY ***

Sign up for WeBull Securities Brokerage and fund any amount to receive up to USD500 in share value (Apple, Tesla, Microsoft, Google)

Receive Free Money (USD30~USD500) When You Sign Up With WeBull Securities Platform (Fund ANY Amount)

*** FREE RESOURCES ***

Keen to learn about options trading but do not wish to pay for expensive courses, this newbie guide will help gain the knowledge and fundamentals to understand options better. And it’s totally free!

The Newbie’s Guide To Options Trading

After accumulating more than 600k of unrealized losses on my portfolio, I wrote this article to encourage friends and investors who are also losing a lot of money to the market.

If You Are Feeling Depressed From Losing Lots Of Money In The Stock Market, Here’s An Article For You

In the 10 years of my investing journey, I have made many mistakes but also learned many lessons from these mistakes. I compiled the 10 most valuable lessons that I have learned and may they help you succeed in your investing journey.

Happy 10 Years Of Investing | 348k (Realised) Profit, 635k (Unrealized) Loss & 10 Lessons Learnt

The precious 6 lessons I learnt after cutting more than half a million of losses in the stock market through bad investments and risky trades.

6 Lessons Learnt After Losing 551k In 10 Years Of Investing & Options Trading | What Newbies Should Know They Start Investing/ Trading

How I managed to build a 1M investment/ trading portfolio despite coming from humble beginnings.

How A Poor Kid Got To A 1M Investment Portfolio | Tips & Principles Of Building Wealth

I did these 10 side hustles while holding a full-time job, so I share them here so you can be inspired to grow your wealth through a side hustle that you enjoy.

I Did These 10 Side Hustles While Working Full Time | 10 Side Hustle Ideas To Help You Earn An Extra Income

Struggling with inflation and high cost of living? Try these 10 methods to help you save money and accumulate more savings for investments or rainy days.

10 Ways To Save Money To Help You Fight Inflation & Rising Costs Of Living

Why I am building $120,000 of cash reserves in Singapore Savings Bonds (SSB) & 5 reasons why I think SSB is a worthy low or zero risk investment that you can consider.

Why I Am Building $120,000 Of Cash Reserves In Singapore Savings Bonds (SSB)? | 5 Reasons Why SSB Is A Worthy Low Risk Investment

Sharing why I am doing Dollar Cost Average (DCA) into SPY and QQQ ETF for long term investments and a step-by-step guide to doing it automatically with Interactive Brokers.

Why I Am Doing DCA (Automatically) For SPY & QQQ For My Long Term Investment? (20% ~ 30% Upside Potential) | Step By Step Guide To Activating Automatic Recurring Investment On IBKR

*** FREE MOTIVATIONAL BOOK ***

If earning more money from your investment does not excite you anymore, you may be seeking a purpose that brings fulfillment and meaning in life. I have written a motivational book that may be useful to you in some ways. You can also download a free copy here:

https://learninginvestmentwithjasoncai.com/finding-the-magical-realm-of-happiness-motivational-book