If you’ve spent any time reading local financial headlines or scrolling through online forums, you’ve probably seen some terrifying retirement numbers thrown around. “You need $3 million to retire!” “No, make it $5 million!” “At this rate, we’ll need $10 million just to survive!”

When you plug these numbers into a generic online retirement calculator, it’s easy to panic. But the biggest mistake most people make in their 40s isn’t that they haven’t saved enough—it’s that they’ve been optimizing toward the wrong retirement number the whole time.

Retirement planning is intensely personal. Let’s throw out the generic formulas and break down how the real math works in Singapore across 5 clear steps.

Step 1: Start with the Lifestyle, Not the Number

Most retirement analyses make a fatal flaw: they start with a massive nest egg number (like $3 million) and work backward. You can’t do that. The ultimate number is the output, which means it completely depends on your input—your desired lifestyle.

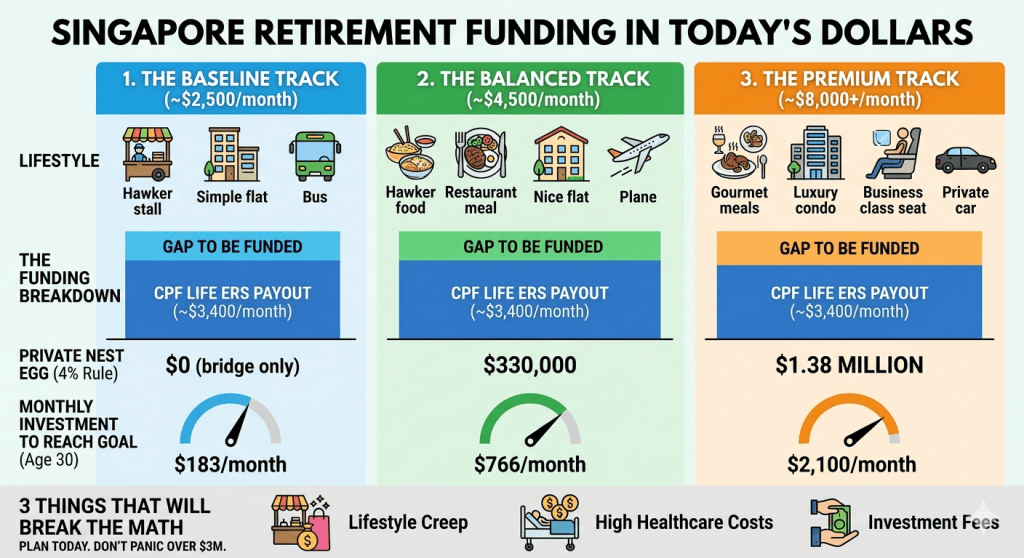

What does retirement actually look like for you? Most Singaporeans fall into one of these three distinct lifestyle tracks (measured in today’s dollars, per person):

- The Baseline Track (~$2,500/month)

- Your HDB flat is fully paid off.

- You eat at hawker centers most days, with the occasional restaurant meal.

- You travel about once a year regionally, keeping to a strict budget (no business class).

- You are reasonably comfortable, but quite careful with daily spending.

- The Balanced Track (~$4,500/month)

- Your HDB flat is paid off.

- You eat out more frequently and travel twice a year, enjoying a mix of regional and long-haul flights.

- You aren’t wasting money, but you aren’t counting every single dollar either.

- You maintain a solid financial buffer for healthcare.

- The Premium Track (~$8,000+/month)

- Regular international travel, sometimes upgrading to business class.

- Full access to private healthcare and potentially maintaining a car.

- Having the financial freedom to fund your grandkids’ education or support family members.

Be honest with yourself about which track you want. A single person’s retirement target can look completely different based purely on these daily expectations.

Step 2: The 4% Rule (Before Government Payouts)

To find our starting benchmark, we look to a classic financial framework: The 4% Safe Withdrawal Rate (originating from the famous Trinity Study).

The premise is simple: if your portfolio is invested in a sensible, diversified mix of stocks and bonds, you can safely withdraw 4% of it in your first year of retirement (and adjust for inflation later) with a very high probability that your money will last at least 30 years.

If we take our annual spending for each track and divide it by 4% (or multiply the annual spend by 25), here is what the raw numbers look like before considering any government benefits:

- Baseline: $750,000

- Balanced: $1.35 Million

- Premium: $2.4 Million

Notice something? Even the Premium track—complete with business class flights and private healthcare—comes out to $2.4 million. It is nowhere near the scary $5 million or $10 million figures people throw around online.

But it gets even better because these figures assume you have zero government payouts.

Step 3: Layering in the Singapore Advantage: CPF Life

This is where standard, imported western retirement calculators completely fail locals because they entirely ignore CPF.

If you live and retire in Singapore, CPF Life acts as a government-guaranteed income stream that pays you every single month from age 65 for the rest of your life—you literally cannot outlive it. Your exact payout depends on whether you hit the Basic (BRS), Full (FRS), or Enhanced Retirement Sum (ERS) by the time you retire.

Let’s focus on the gold standard: the Enhanced Retirement Sum (ERS). If you can maximize your Retirement Account to the ERS by age 65, CPF Life (under the Standard Plan) will pay you roughly $3,400 a month for life. That is a guaranteed ~$40,000 a year.

When you subtract this guaranteed $3,400/month from your desired lifestyle tracks, the actual amount you need to save in a private investment portfolio drops drastically:

- Baseline Track ($2,500/mo needed): Your CPF Life ERS payout ($3,400/mo) already completely covers it. In theory, your retirement nest egg outside of CPF can be close to zero—you just need enough cash to bridge the gap years between when you stop working and when CPF Life kicks in at age 65.

- Balanced Track ($4,500/mo needed): After subtracting CPF Life, your private portfolio only needs to cover a $1,100/mo gap. Using the 4% rule, you only need ~$330,000 invested outside of CPF. Not $3 million. Not $5 million. Just $330,000.

- Premium Track ($8,000/mo needed): Your private portfolio needs to bridge a $4,600/mo gap. This requires ~$1.38 Million invested outside of CPF.

(Note: These are calculated in today’s dollars. The nominal amounts will be higher in the future due to inflation, which is why we must invest in assets that grow with and outpace inflation).

Step 4: What You Need to Invest Every Month (By Age)

Knowing the destination is great, but how do we build the bridge to get there?

Let’s look at the monthly contributions required to hit those cash targets ($330k for Balanced, $1.38M for Premium) assuming a conservative 7% nominal annual return from investing in low-cost, globally diversified ETFs.

If you start at Age 30:

- To reach the Balanced Track: You only need to invest $183 a month. That is less than what the average person spends on food delivery apps or just two ride-hailing trips a week.

- To reach the Premium Track: You need to invest $766 a month. While that is real money, it’s completely achievable for a dual-income household without radically altering their lifestyle—you don’t need a massive corporate salary to achieve it.

The math is incredibly reasonable. The retirement system is fundamentally built to make this work. The system only “fails” because people wait until they are in their late 30s or 40s to start. When you delay, compounding works against you, and your required monthly investment shoots up drastically.

Step 5: Three Things That Will Break the Math

While the math is clean on paper, life is messy. There are three major traps that can completely derail your retirement calculations if you aren’t careful:

- Lifestyle Creep: A $4,500 monthly retirement budget only works if you are actually content with a $4,500 lifestyle. If you are actively spending $10,000 a month on non-essentials in your 40s, you will not magically be happy living on less than half of that at age 65. Plan honestly and lean toward conservative assumptions.

- Healthcare Scenarios: Local healthcare is world-class, but it isn’t free. If you prefer private hospitals and specialist care, your medical costs in the final two decades of your life can spike aggressively. Ensure your Integrated Shield Plan is locked down, your CareShield Life is upgraded if appropriate, and you have built a strict buffer above your baseline numbers.

- Investment Fees: Fees compound over time exactly like returns do. Paying a 2% management fee on an Investment-Linked Policy (ILP), a high-fee robo-advisor, or an actively managed portfolio—as opposed to a 0.2% fee on a low-cost ETF—can wipe out 30% to 40% of your total wealth over a 35-year runway. Fix your fees first by using low-cost ETFs through global, affordable brokerages.

The Bottom Line

Stop stressing over whether you need $3 million or $5 million to survive. Instead:

- Identify your realistic lifestyle track.

- Layer in your projected CPF Life payouts (whether BRS, FRS, or ERS).

- Calculate the actual financial gap left over and break it down into a monthly savings goal.

The hardest part of retirement planning isn’t running the math—it’s simply having the discipline to start putting your money to work.

Credits: Tim Talks Money

*** SEE MY TRADES & PORTFOLIO ON PATREON ***

If you are interested to find out more about my options trades and investment portfolio, I will be updating them on Patreon (on the same day I made the trades), so do follow me there if you need some reference or inspiration.

Click here to access my Patreon page

*** FOLLOW US ON SOCIAL MEDIA ***

Follow me on Facebook and LinkedIn, to get notified of my latest posts on social media. Or subscribe to my blog (scroll to the bottom of the page) to have my new posts sent directly to your mailbox.

We also have a community passionate about investing, trading, and personal finance over our Telegram or Facebook group. So, join us there for a good discussion, post queries, or simply share your financial knowledge.

*** FREE BEGINNER GUIDE TO OPTIONS TRADING ***

Keen to learn about options trading but do not wish to pay for expensive courses, this newbie guide will help gain the knowledge and fundamentals to understand options better. And it’s totally free!

The Newbie’s Guide To Options Trading

*** FREE MOTIVATIONAL BOOK ***

If earning more money from your investment does not excite you anymore, you may be seeking a purpose that brings fulfillment and meaning in life. I have written a motivational book that may be useful to you in some ways.

Click here to download my motivational book

*** BUY ME A CUP OF COFFEE ***

If my blog has benefited you in some ways and you would like to offer a token of appreciation, you may do so via this page. Thank you very much for your support!

Click here to support the site

*** MUST-READ BLOG POSTS ***

The day that I lost everything….

I Was Margin Called, IBKR Liquidated ALL My Positions & Realised S$540k (USD400k) Worth Of Losses

Sharing these 6 fatal mistakes in investing and options trading so you can avoid these pitfalls

The 6 Fatal Investing/ Trading Mistakes That Made Me Lose More Than $1M

After accumulating more than 600k of unrealized losses on my portfolio, I wrote this article to encourage friends and investors who are also losing a lot of money to the market.

If You Are Feeling Depressed From Losing Lots Of Money In The Stock Market, Here’s An Article For You

The precious 6 lessons I learnt after cutting more than half a million of losses in the stock market through bad investments and risky trades.

6 Lessons Learnt After Losing 551k In 10 Years Of Investing & Options Trading | What Newbies Should Know They Start Investing/ Trading

In the 10 years of my investing journey, I have made many mistakes but also learned many lessons from these mistakes. I compiled the 10 most valuable lessons that I have learned and may they help you succeed in your investing journey.

Happy 10 Years Of Investing | 348k (Realised) Profit, 635k (Unrealized) Loss & 10 Lessons Learnt

How I managed to build a 1M investment/ trading portfolio despite coming from humble beginnings.

How A Poor Kid Got To A 1M Investment Portfolio | Tips & Principles Of Building Wealth

I did these 10 side hustles while holding a full-time job, so I share them here so you can be inspired to grow your wealth through a side hustle that you enjoy.

I Did These 10 Side Hustles While Working Full Time | 10 Side Hustle Ideas To Help You Earn An Extra Income

Struggling with inflation and high cost of living? Try these 10 methods to help you save money and accumulate more savings for investments or rainy days.

10 Ways To Save Money To Help You Fight Inflation & Rising Costs Of Living

Why I am building $120,000 of cash reserves in Singapore Savings Bonds (SSB) & 5 reasons why I think SSB is a worthy low or zero-risk investment that you can consider.

Why I Am Building $120,000 Of Cash Reserves In Singapore Savings Bonds (SSB)? | 5 Reasons Why SSB Is A Worthy Low-Risk Investment