Most of us have this trusted insurance agent whom we met at a certain stage of our life. They double up as our financial planners who can help us grow our wealth through the different saving/ investment-linked plans offered by their companies.

Despite keeping the leap of faith that these financial planners will have your best interest at heart, I thought it is a good idea to always verify the plan that your agent recommends to you. In this article, I would like to share a personal experience to prove this point.

The Story Begins

My mum had some saving plans from her insurance company maturing and she could free up the capital and interest earned on these policies. I told her that she could consider Singapore Saving Bonds (SSB) as the 10-year average annual return is more than 2.6%.

I told her the other advantages of investing in SSB, such as it is capital and interest guaranteed and she could withdraw in any period she wanted and the payout would come the following month.

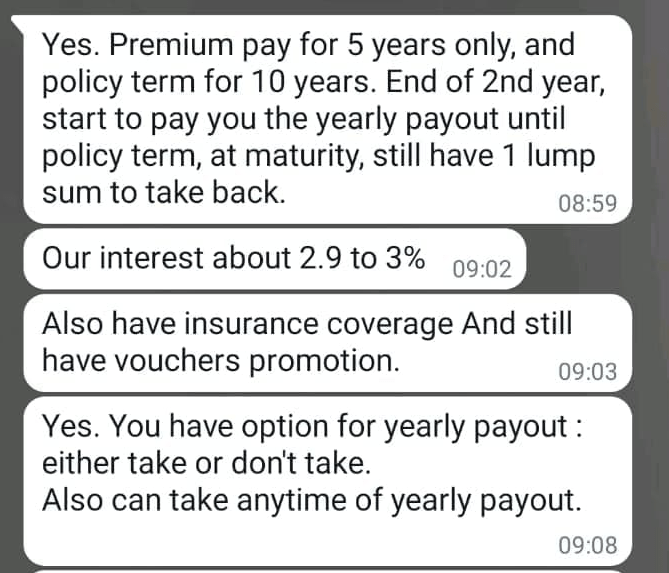

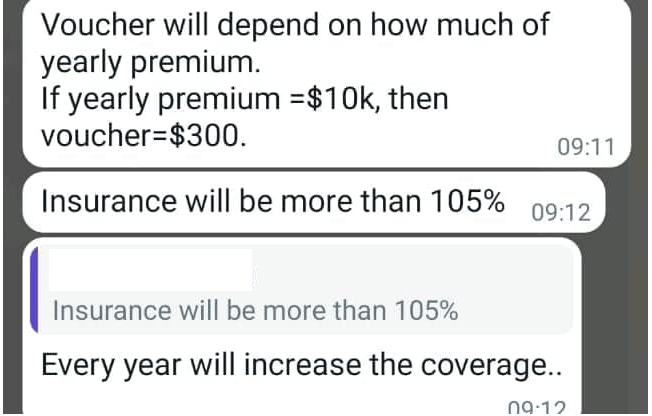

Her insurance agent, who has been serving her for decades, told her that the insurance company can offer a better option, a plan which offers a good interest rate, can withdraw anytime, and has insurance coverage as well. Upon signing up, she can also get some supermarket vouchers.

This is what he (insurance agent) said:

So, I am also keen to find out more about this plan that is supposedly better than SSB.

There are 2 types of saving plans offered by the insurance company, but both plans will require her (my mum) to deposit $10,000 annually for the first 5 years, up to a total capital of $50,000. Thereafter, the plans will continue to run their courses until they reach maturity at the 10th year.

The first plan allows her to do an withdrawal amount of $1,729 every year starting from the end of the 2nd year, i.e. from year 2 to year 10, while the second plan allows her to withdraw her money anytime. For context, my mum is 65 years old and a non-smoker.

Deep Dive Into The 2 Saving Plans

Let’s start off with the first plan that has the yearly payout of $1,729, starting from the end of 2nd year.

This is the illustration table for the death compensation aka the insurance component, in the event the policy holder passed away before the policy ends.

For the 1st year, the payout from insurance is $10,321, which is 103.21% of the $10,000 capital invested into this plan. For 2nd year, it is also at 103.21% (20,642 divide by 20,000). By 3rd year, it is at 105.26% and at 4th year, it is at 105.65%. At 5th year, it is 106.1%.

I am taking the numbers from the best case scenario where the investment return of the company is projected at 4.25%. For other projection, the yield is lower.

To cross check against the agent’s claim, the 105% coverage is only true on the 3rd year policy instead of straight from the start (based on the 4.25% project investment return). The other claim on the % of coverage increasing every year is true.

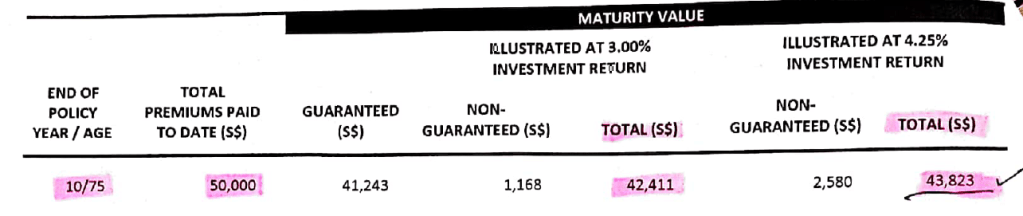

At 10th year, the maturity value is as follow:

After 10 years, the yearly payout accumulated from Year 2 to Year 10 will be $15,561 (1,729 x9).

If we do apple-to-apple comparison with the guaranteed maturity value, it will be $41,243 + $15,561 = $56,804, which is 13.6% gain over 10 years, which average out to 1.36% per annum.

If we take the best case scenario, where projected investment return is at 4.25%, then the total return will be $43,823 + $15,561 = $59,384, which a 18.7% gain over 10 years, which average out to 1.87% per year.

This 10-year average is still lower than what Singapore Savings Bond is offering at 2.6% in June 2022, which July’s bond is at 2.71%.

Second Plan (Withdraw Anytime)

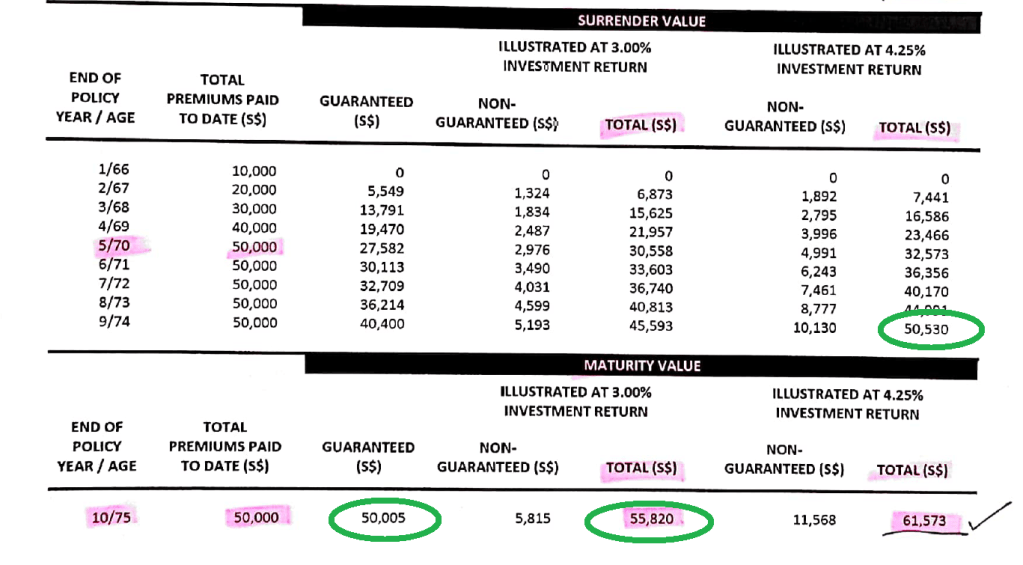

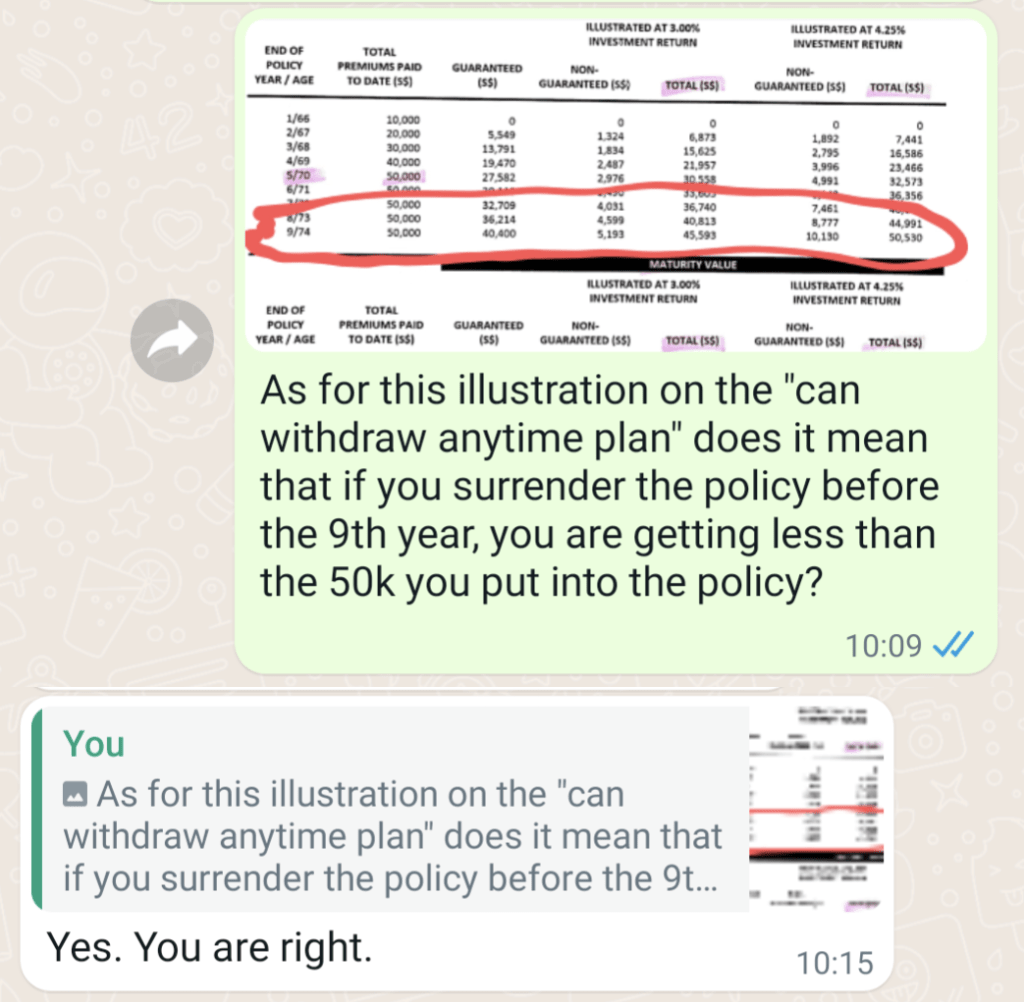

This is the illustration for second plan:

If my mum does not withdraw any money for 10 years, she will get $61,573 based on the best case scenario (projected 4.25% investment return), that translate to a 23.1% return over 10 years, and an average of 2.31% per annum, which is comparable to Singapore Savings Bond at an average of 2.6% per annum.

However, if you were to compare with the guaranteed returns, it is at $50,005, which is barely earning anything over 10 years.

One point that the agent did not mention or conveniently forgot to mention is the surrender value over the years. He mentioned that this plan is as flexible as the Singapore Savings Bonds where you can choose to terminate anytime during the 10 years.

However, if my mum terminates her plan before the 9th year (for the best case scenario), she will not reach breakeven on her capital, which means that not only is she not earning any interest for the number of years (1 to 8 years) she parked her money in this plan , she will still lose a portion of her capital. See green circles above for the breakeven amouns and their corresponding year.

So, I clarified this with the agent:

Concluding Thought

I feel that as compared to SSB, the good thing about this plan is that you do not need to upfront deposit $50,000 into the plan and you can progressively reach this amount in 5 years. However, that is not the objective of this post.

In this post, I just want to remind everyone to do your due diligence to look through your insurance plan and see if it makes sense to you, instead of outsourcing your responsibility of managing your personal finance to your trusted insurance agent cum financial planner. They may have told you all the great things about the plan and conveniently forgot to mention the caveat/ catch.

In the above example, the agent mentioned about good thing about being able to do yearly withdrawal but did not mention that after doing that, the average interest rate over 10 years is low. He also mentioned about good thing about the second plan of being able to withdraw anytime, but did not mention that by doing so, you are withdrawing at a loss.

*** FREE RESOURCES ***

Keen to learn about options trading but do not wish to pay for expensive courses, this newbie guide will help gain the knowledge and fundamentals to understand options better. And it’s totally free!

The Newbie’s Guide To Options Trading

Looking for ideas on what stocks to invest in or which stocks to trade? You can take reference from what I have been buying or selling. I try to update them as soon as I can in this section, as well as share my thoughts on executing these trades:

MY TRADES

If the bear market in 2022 is making feel depressed as your stocks come tumbling down, read this article to find out how you can use options trading to help you claw back some of your losses as you await market recovery:

How I Do Earn Even When The Stock Market Is Bearish?

Also, check out my trading strategies in different market conditions, whether it is bullish, bearish or volatile:

How Not To Lose Money In Trading? | My Trading Strategies For Bullish, Bearish And Volatile Market

I watched tons of videos on YouTube since 2020 and if you are wondering if there are any useful channels that you can subscribe to for learning market trends, TA, FA, check out this compilation here:

My Secret Weapons For Options Trading: I Watch These YouTube Financial Channels Every Day

I concluded my first year of options trading with more than USD160k of gain, see how I do it and the capital I use for every month to give you a sensing of the percentage yield I get out of my gains:

1st Year Options Trading Recap: The Journey Towards SGD$217,509 Profits In 2021

This blog is as authentic and as transparent as I can share, I do not just show the wins and hide the loss. I have made some very bad decisions in the first 8 years of investing and paid a huge price for them. Here is the loss I have accumulated during these years. I hope you learn some lessons from my mistakes.

I Cut $135,715 Worth Of Losses In The Last 1.5 Months

Want to learn more about Technical Analysis (TA) but find it difficult to grasp the concepts? This article brings you TA at a glance, and helps you understand key terminologies, indicators, and techniques used in TA to equip you with the knowledge that can empower you in your investing/ trading journey.

The Newbie Guide To Technical Analysis (TA)

Excited to start your trading journey or perhaps try out with a paper trading account to build your confidence in trading? Check out this step-by-step to help you get started:

How To Buy Options on Interactive Brokers (Step-By-Step)

Follow me on your favorite social media platforms, Facebook, LinkedIn, or Twitter, to get notified of my latest blog posts. Or join our investing/ trading community at Telegram to exchange ideas or ask questions relating to investing/ trading.

Hi Jason, I am following your option trades on your blog and as well as on Facebook.

I am a FA Rep (Financisl Advisory Rep, currently representing at least 10 different life insurers) for the past 22yrs and a Direct Insurance Agt for the even earlier 10yrs.

I have come across many agents that choose to conveniently leave out crucial important information in their “pitch” to their customers. Granted sometimes customers do get the wrong impression of certain facts but it is still the duty & obligation of the agent to convey and ensure that the important and salient facts are communicated & understood, and especially in recent times, documented, seen and signed by the client – this is a practice that FA Reps in my previous firm and current firm were/are doing. Probably it is very important at our end as we do product comparisons for our customers, and they make the final choice/decision.

For your mom’s case, due to her age, she is deemed as “Vulnerable Clients” in the industry. If she doesn’t understand English or have a low education level, it exacerbates her Vulnerable Client status.

You have certain options open to you, if you are keen to pursue a refund, or use the Free Look period (even though it may have lapsed). Contact me directly if you are keen to pursue these options and I’ll try to help you in my best capability.

LikeLike

Hi Ang, thanks so much for reaching out and providing such valuable info. Really glad to hear about the good work that you and your team are doing. I will get in touch with you if I need to follow up on my mum’s policies. Please continue to keep up the good work!

LikeLike

No worries, Jason. Most happy to help, if required.

LikeLike