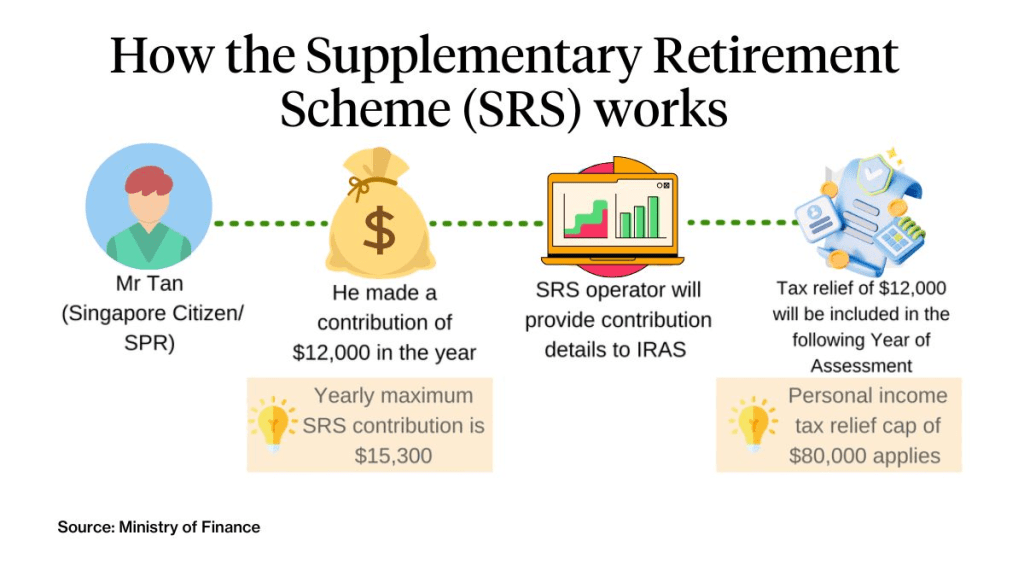

When it comes to retirement planning in Singapore, the tools we have are powerful—if you know how to sequence them correctly. Recently, I’ve been getting some questions from readers about how I’m structuring my own nest egg, so today I want to break down exactly why I chose to top up around $15,000 (hitting the $15,300 cap for locals) into my Supplementary Retirement Scheme (SRS) account last year and will continue to do so this year.

The topping up of my SRS is part of the three-stage strategy that optimizes tax relief today while building a bulletproof income bridge for the future.

Here is the exact playbook.

The Immediate Win: Slicing Through the Tax Bracket

First, let’s talk about the immediate, guaranteed return on investment.

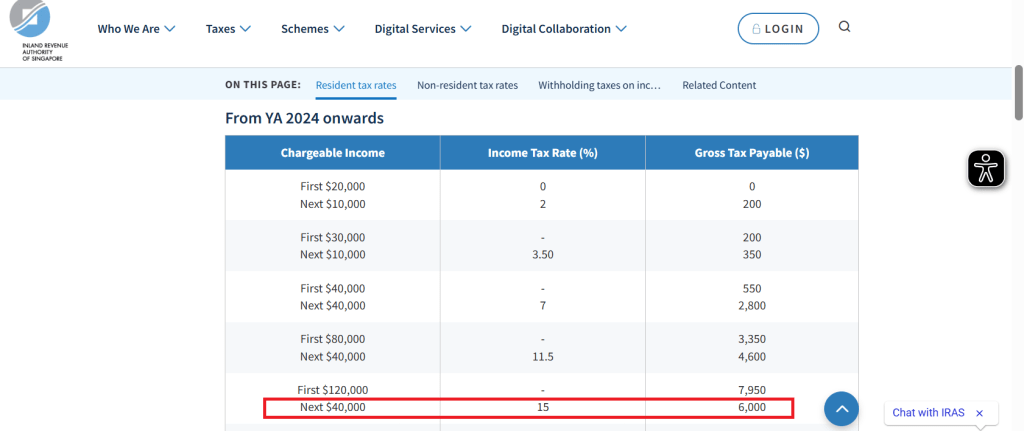

The most immediate benefit of the SRS is direct tax relief. Every dollar you contribute to your SRS account reduces your chargeable income by that exact same amount for the Year of Assessment (YA). The below table shows the income tax rate for the various income brackets.

If you are a high income earner, with taxable income ranging between $120,000 and $160,000, your marginal tax rate jumps to 15%. That means every dollar you earn above that threshold is taxed at a noticeable premium. By funneling $15,300 into my SRS account, I am directly reducing my chargeable income.

At the 15% tax bracket, a $15,300 top-up translates to an immediate tax savings of $2,295, i.e. you pay less this amount of income tax the following year. In the investing world, finding a guaranteed 15% “yield” on day one is incredibly rare. The SRS top-up locks that in instantly, keeping more of my hard-earned money working for my own portfolio rather than going straight to the taxman.

But the tax relief is just the appetizer. The real magic of the SRS account shines when integrated into a long-term withdrawal timeline. Here is how I plan to sequence my payouts from age 55 to 70 and beyond.

Stage 1: Age 55 – Unlocking the CPF Ordinary Account

At age 55, the first milestone of Singapore’s retirement framework kicks in. Once my Retirement Account (RA) is formed and the Full Retirement Sum is set aside, the remaining balances in my Ordinary Account (OA) become liquid. The OA account acts like a bank account offering guaranteed 2.5% per annum interest for whatever amount is inside the account.

This is the first phase of my withdrawal strategy. I plan to tap into my available OA funds to supplement my lifestyle and cover expenses. Because these funds have already compounded at stable rates for decades, they serve as a reliable first pillar to lean on during my mid-50s to early 60s, allowing my other investments to remain untouched and continue compounding.

Stage 2: Age 63 – The 10-Year SRS Income Bridge

At age 63 (the current statutory retirement age), Stage 2 begins. This is where the SRS funds I’m building up right now come into play.

The beauty of the SRS is the 10-year withdrawal window. When you withdraw your SRS funds upon reaching the statutory retirement age, only 50% of the withdrawal is subject to tax.

If I pace the withdrawals evenly over 10 years and keep the 50% taxable portion below the $20,000 threshold (where the Singapore tax rate is 0%), i.e. withdraw I can withdraw $40,000 per year from my SRS account and do not need to pay any tax.

I can effectively draw down my entire SRS portfolio completely tax-free. This SRS income stream forms a perfect, tax-optimized 10-year bridge that comfortably carries me from age 63 right up to age 70.

Stage 3: Age 70 – Maximizing CPF LIFE

Why use the SRS to build a bridge to 70? Because it allows me to delay my CPF LIFE payouts.

While you can start receiving CPF LIFE payouts at 65, deferring it is one of the most powerful moves you can make. For every year you defer your CPF LIFE payouts up to age 70, your monthly payouts increase by up to 7%. By relying on my SRS funds from 63 to 70, I can comfortably delay CPF LIFE for the full five years.

By the time I turn 70, those CPF LIFE payouts will have grown by roughly 35%, locking in a significantly higher, guaranteed monthly income stream for the rest of my life.

Concluding Thoughts

Retirement planning isn’t just about putting money away; it’s about cash flow management across different decades of your life. Because if we do that, we no longer need to keep chasing that “1M” milestone and then not knowing how to manage that amount properly.

By spacing out my payout starting from OA to SRS to CPF Life, I can possibly retire earlier at the age of 55, which is my target retirement age.

Topping up $15k into my SRS isn’t locking my money away—it’s buying me an immediate 15% tax discount today, and funding a strategic 10-year bridge tomorrow so that my ultimate CPF LIFE payouts can compound to their absolute maximum limit.

*** FOLLOW US ON SOCIAL MEDIA ***

Follow me on Facebook and LinkedIn, to get notified of my latest posts on social media. Or subscribe to my blog (scroll to the bottom of the page) to have my new posts sent directly to your mailbox.

We also have a community passionate about investing, trading, and personal finance over our Telegram or Facebook group. So, join us there for a good discussion, post queries, or simply share your financial knowledge.

*** SEE MY TRADES & PORTFOLIO ON PATREON ***

If you are interested to find out more about my options trades and investment portfolio, I will be updating them on Patreon (on the same day I made the trades), so do follow me there if you need some reference or inspiration.

Click here to access my Patreon page

*** FREE BEGINNER GUIDE TO OPTIONS TRADING ***

Keen to learn about options trading but do not wish to pay for expensive courses, this newbie guide will help gain the knowledge and fundamentals to understand options better. And it’s totally free!

The Newbie’s Guide To Options Trading

*** FREE MOTIVATIONAL BOOK ***

If earning more money from your investment does not excite you anymore, you may be seeking a purpose that brings fulfillment and meaning in life. I have written a motivational book that may be useful to you in some ways.

Click here to download my motivational book

*** BUY ME A CUP OF COFFEE ***

If my blog has benefited you in some ways and you would like to offer a token of appreciation, you may do so via this page. Thank you very much for your support!

Click here to support the site

*** MUST-READ BLOG POSTS ***

The day that I lost everything….

I Was Margin Called, IBKR Liquidated ALL My Positions & Realised S$540k (USD400k) Worth Of Losses

Sharing these 6 fatal mistakes in investing and options trading so you can avoid these pitfalls

The 6 Fatal Investing/ Trading Mistakes That Made Me Lose More Than $1M

After accumulating more than 600k of unrealized losses on my portfolio, I wrote this article to encourage friends and investors who are also losing a lot of money to the market.

If You Are Feeling Depressed From Losing Lots Of Money In The Stock Market, Here’s An Article For You

The precious 6 lessons I learnt after cutting more than half a million of losses in the stock market through bad investments and risky trades.

6 Lessons Learnt After Losing 551k In 10 Years Of Investing & Options Trading | What Newbies Should Know They Start Investing/ Trading

In the 10 years of my investing journey, I have made many mistakes but also learned many lessons from these mistakes. I compiled the 10 most valuable lessons that I have learned and may they help you succeed in your investing journey.

Happy 10 Years Of Investing | 348k (Realised) Profit, 635k (Unrealized) Loss & 10 Lessons Learnt

How I managed to build a 1M investment/ trading portfolio despite coming from humble beginnings.

How A Poor Kid Got To A 1M Investment Portfolio | Tips & Principles Of Building Wealth

I did these 10 side hustles while holding a full-time job, so I share them here so you can be inspired to grow your wealth through a side hustle that you enjoy.

I Did These 10 Side Hustles While Working Full Time | 10 Side Hustle Ideas To Help You Earn An Extra Income

Struggling with inflation and high cost of living? Try these 10 methods to help you save money and accumulate more savings for investments or rainy days.

10 Ways To Save Money To Help You Fight Inflation & Rising Costs Of Living

Why I am building $120,000 of cash reserves in Singapore Savings Bonds (SSB) & 5 reasons why I think SSB is a worthy low or zero-risk investment that you can consider.

Why I Am Building $120,000 Of Cash Reserves In Singapore Savings Bonds (SSB)? | 5 Reasons Why SSB Is A Worthy Low-Risk Investment